SUBMISSION OF FINANCIAL STATEMENTS – SUSPENDED DEADLINE FOR SUBMISSION

The amendments to the Accounting Act (OG 42/2020 dated 7 April 2020), received an epilogue on 8 April 2020 in the form of amendments to the Ordinance on deadlines for the submission of financial statements and accounting documentation under special circumstances (OG 43/2020 dated 8 April 2020). The amendments were initiated by numerous associations of accounting employees and accountants, who have been under considerable pressure in recent weeks to apply to various measures for their clients, to monitor numerous amendments in recent weeks and to work on the final financial statements of clients under special circumstances involving restricted movement as well as circulation of documentation.

The Ordinance prescribes new deadlines for the duration of these special circumstances:

It is also important to note that liabilities regarding public levies established on the basis of the Income Tax Return, forms and reports are due on 31 July 2020.

These provisions shall not apply to taxpayers whose tax period is not equated with the calendar year in accordance with a special regulation on income taxation (initiating bankruptcy, status changes, discontinuation of business, etc.), i.e. whose obligation to file an Income Tax Return is not due 4 months after the tax period expires.

Job preservation measures – UPDATE

On 07 April 2020, the Croatian Employment Service published a third version of the job preservation measures. The latest changes are the product of the last week’s announcement by the Government of the Republic of Croatia regarding the increase of the job preservation fee from HRK 3250 to HRK 4000, as well as a better definition of situations that had remained unresolved in the previous provisions.

The key changes to this grant are as follows:

- Employees of branch offices and representative offices of foreign companies in the Republic of Croatia are defined in the group of workers who can be included in the implementation of this grant. So far, this measure has focused exclusively on employees of Croatian legal entities. The circle of beneficiaries of this grant has also been extended to include companies under liquidation and bankruptcy, provided that they have employees and regularly meet their obligations;

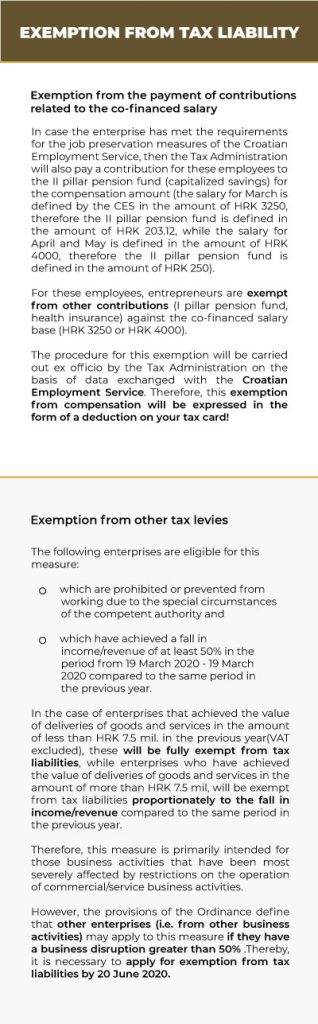

- the grant amount for March 2020 shall remain HRK 3250/employee, but the fee amount for the months of April and May 2020 shall be increased to HRK 4000/employee (for full-time);

- the news is that, based on this grant, the Tax Administration will make a contribution payment (II pillar pension fund) of HRK 203.12 for March 2020, i.e. HRK 250 for April and May 2020 (i.e. 5% at the converted rate for the II pillar pension fund).In this manner, the fact that net salary financing implies adequate payment to the employee in the II pillar pension fund is resolved;

- Due to the fact that a part of, primarily, commercial premises was closed by the Decision of the Civil Protection Headquarters, a part of the employers decided to terminate employment contracts with traders in the initial phase. The new version of this measure states that employers may also use the measures for these employees whose employment had been terminated, but have been re-employed (during the period from 1 March to 1 April 2020).The only requirement for realizing these rights is that the employee had not exercise their right to unemployment benefits during unemployment. In the event that an employee had received unemployment benefits for March 2020, the employer is entitled to cash compensation for this employee for April and May 2020;

- The deadlines for the submission of a grant application by an

enterprise have been defined, namely:

- for the payment of salary costs for April and May – deadline 5 May 2020;

- for the payment of salary costs for May – deadline 7 July 2020.

- In principle, compensation cannot be obtained for owners co-owners, founders, board members, directors and procurators, except in the situation of micro enterprises (i.e. enterprises employing fewer than 10 workers).The latest version states that grants cannot be approved for a co-owner – natural entity in relation to these micro enterprises cannot be granted, if they have more than a 25% share in another legal entity.

Link to the latest text of the COVID 19 job preservation measures: https://mjera-orm.hzz.hr/media/avch5x45/hzz-provedbena-dokumentacija-potpora-za-ocuvanje-radnih-mjesta-koronavirus-060420.pdf

Deferral and exemption from tax levies

Following the amendments to the General Tax Act (OG 42/2020 dated 7 April 2020) adopted yesterday, the Amendments to the Ordinance on the Implementation of the General Tax Act were also published on 8 April 2020 (OG 43/2020 dated 8 April 2020). These amendments are complementary to the first set of measures of the Government of the Republic of Croatia, i.e. the published amendments to the Ordinance on the Implementation of the General Tax Act (OG 35/2020 dated 19 March 2020).

When summarizing these provisions, we can conclude that the measures can be divided into two key areas:

- deferral of tax levies;

- exemption from tax levies.

A recapitulation of the new and previously adopted measures is given below:

We would like to draw your attention to the fact that the provisions of the Ordinance also define the possibility of subsequent control by the tax authority, and that the Tax Administration can abolish the deferral of payment of tax levies followed by a calculation of default interest on late payments of tax liabilities in certain situations. This applies if the enterprises:

- present false facts in reasoning their applications;

- act contrary to tax regulations;

- misuse the tax payment measures to obtain unlawful material gain.

Among other provisions, it is important to state that all deliveries, in the period from 1 April 2020 to 1 July 2020, related to procurement of equipment necessary for the fight against the COVID 19 pandemic from donations will be exempt from VAT .The above-mentioned complies with the measures in other countries, which temporarily exempted from VAT all procurement of goods financed from donations during the fight against the pandemic. The situation is identical with VAT when importing goods needed for the fight against COVID 19.